We analyze premium changes by considering the 9:15 AM values of both Call (CE) and Put (PE) options. This helps in identifying market trends, sentiment shifts, and potential price movements based on the early trading session's option pricing dynamics.

Premium Change Analysis

Premium Change analysis provides traders with real-time insights into how options premiums evolve throughout the trading day. By tracking premium movements against a 9:15 AM baseline, traders can identify optimal entry and exit points while monitoring the combined effects of time decay, volatility changes, and underlying price movements.

Baseline Reference Point

9:15 AM Baseline: All premium changes are calculated relative to the opening premium at 9:15 AM, providing a consistent reference point for intraday analysis. This baseline helps traders understand how much premium has been gained or lost since market open, accounting for overnight changes and early morning volatility.

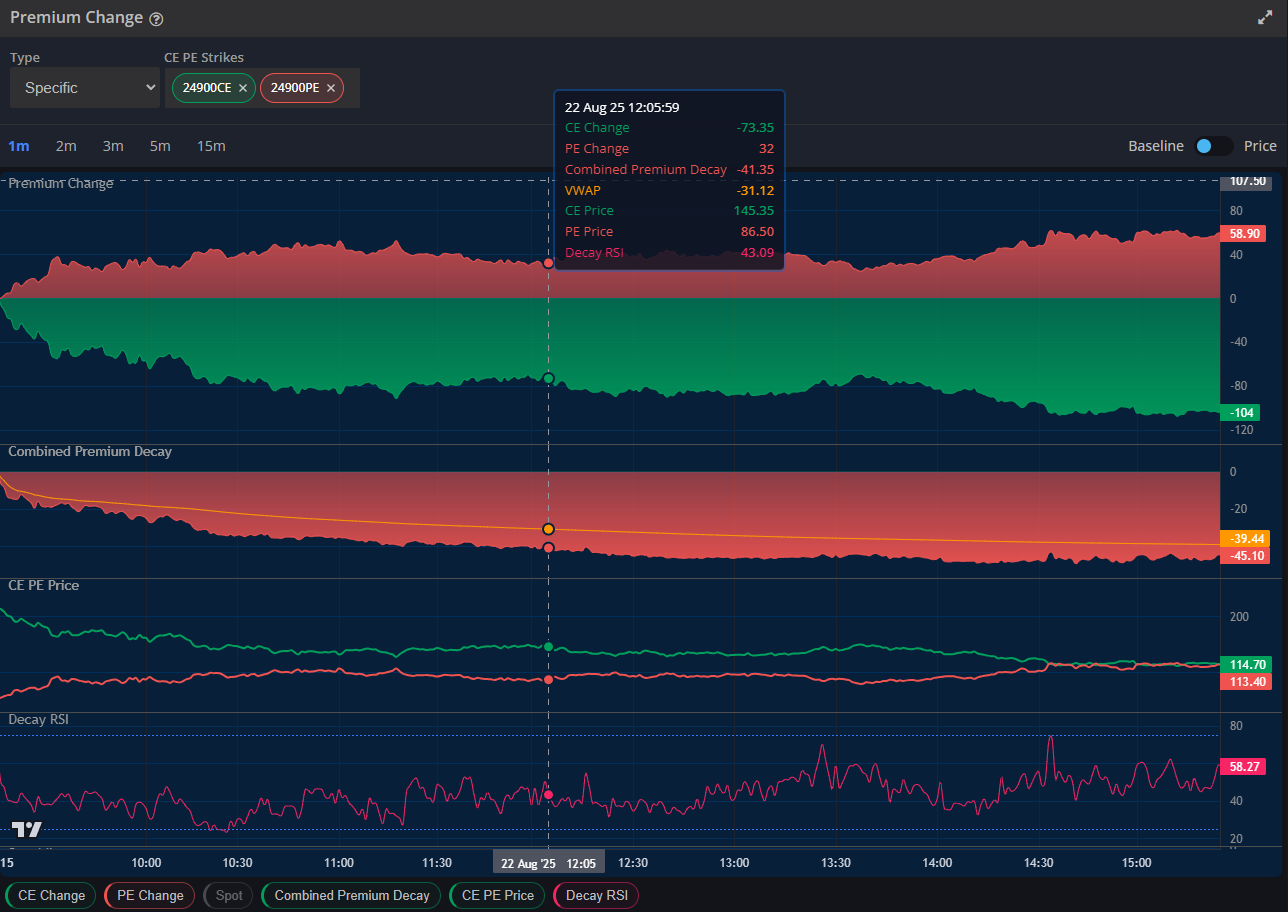

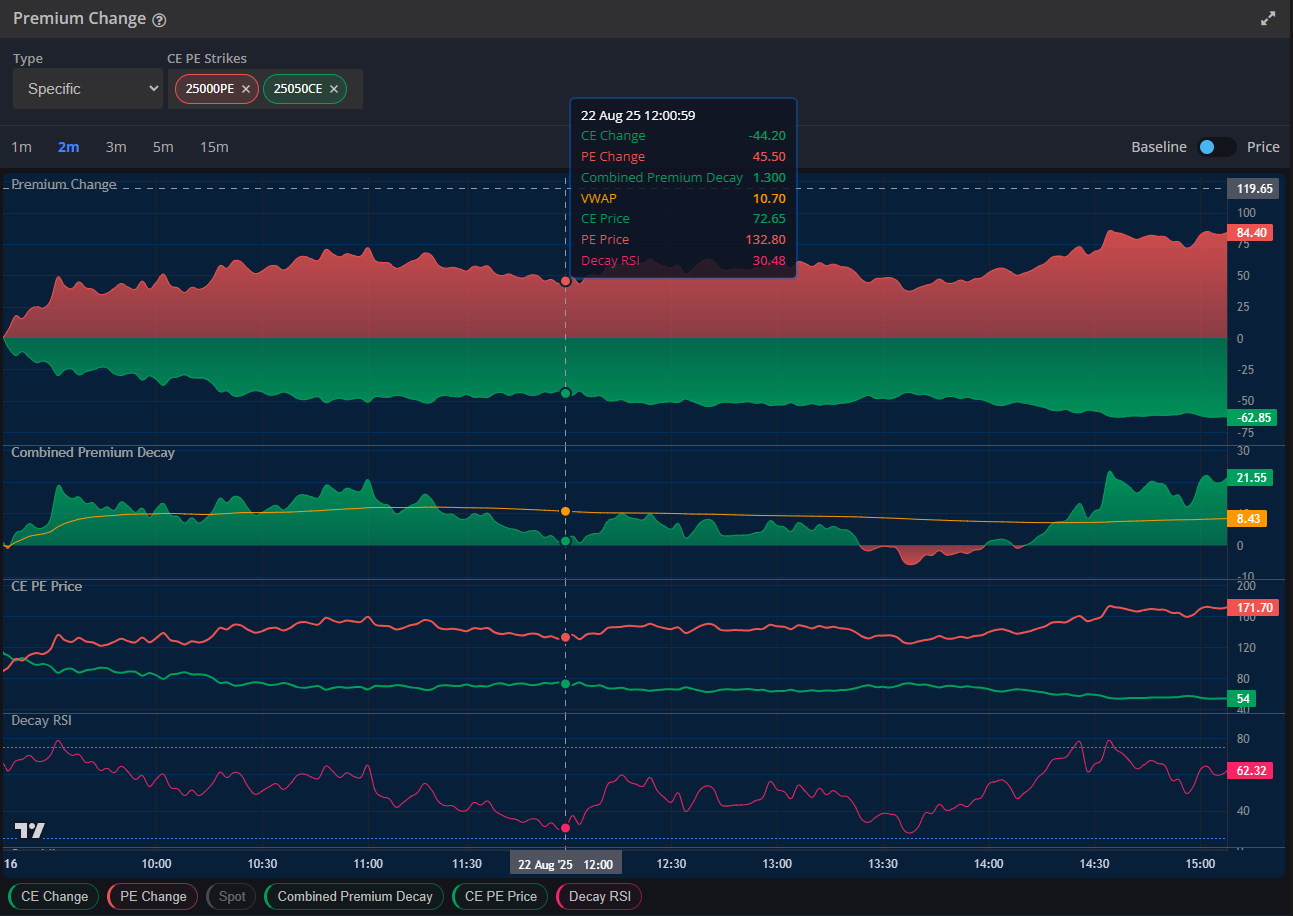

Premium Decay Change: RSI, CE PE Price, Decay linePremium Decay Change: Premium increase and decrease

Understanding Premium Change Components

Premium Change analysis breaks down the complex factors affecting options pricing into measurable components. Each element contributes to the overall premium movement, and understanding their individual impacts helps traders make more informed decisions.

Component

Description

Impact on Premium

Measurement Method

CE Change

Call option premium change from baseline

Positive when calls gain value

Current CE Price - 9:15 AM CE Price

PE Change

Put option premium change from baseline

Positive when puts gain value

Current PE Price - 9:15 AM PE Price

Combined Premium Decay

Time decay effect on both options

Always negative, accelerates near expiry

Theoretical decay from time passage

VWAP Reference

Volume-weighted average price baseline

Shows institutional interest levels

Cumulative volume-weighted pricing

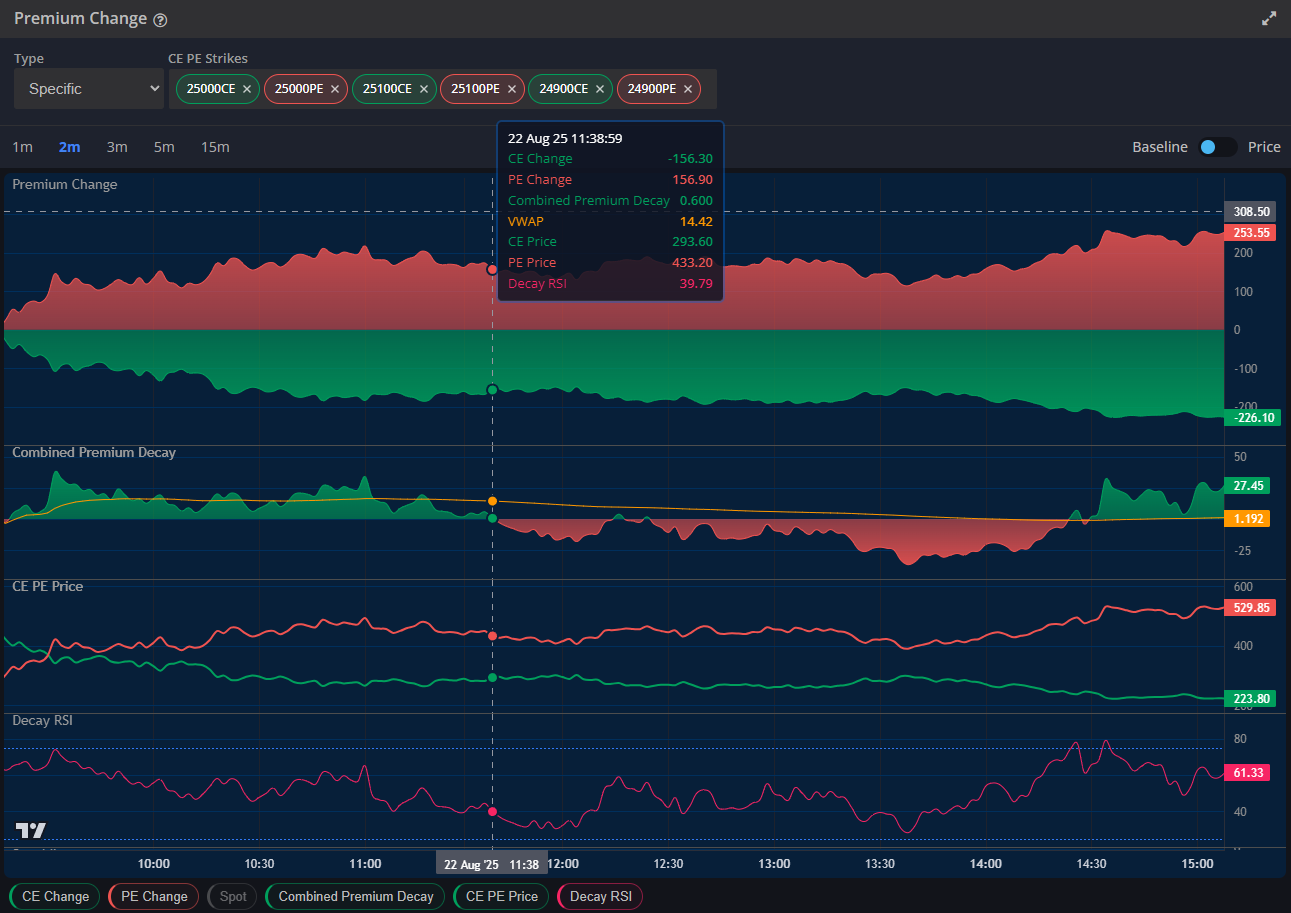

Premium Decay Change: Multi Strikes select

Interpreting Premium Change Patterns

Different premium change patterns reveal important market dynamics. Traders can use these patterns to identify potential trading opportunities and manage existing positions more effectively.

Directional Movement Impact: When the underlying moves significantly, one side of the straddle/strangle gains while the other loses, creating asymmetric premium changes

Time Decay Acceleration: As expiration approaches, time decay becomes more pronounced, especially in the final weeks before expiry

Volatility Expansion/Contraction: Changes in implied volatility affect both call and put premiums simultaneously, often overriding directional effects

Intraday Volatility Patterns: Opening and closing hours typically show higher volatility, while mid-day sessions often experience lower premium fluctuations

Combined Premium Decay Analysis

The Combined Premium Decay metric tracks the theoretical time decay affecting both call and put options simultaneously. This measurement helps traders understand how much premium is lost purely due to the passage of time, independent of price or volatility changes.

Time Decay Insight: Combined Premium Decay accelerates exponentially as expiration approaches. The final week before expiry can see dramatic acceleration in decay rates, especially for at-the-money options.

Decay Rate Factors

Days to Expiration: Options with fewer days to expiry experience faster time decay, following a non-linear acceleration pattern

Moneyness Impact: At-the-money options experience the highest time decay rates, while deep in-the-money or out-of-the-money options decay more slowly

Volatility Environment: High volatility environments can partially offset time decay through increased option values

Interest Rate Effects: Changes in risk-free rates can affect the theoretical decay calculations, though typically minimal for short-term options

Combined Premium Decay RSI

Decay RSI Interpretation: The RSI applied to Combined Premium Decay helps identify when time decay effects are extreme relative to recent patterns. Values above 70 suggest accelerated decay periods, while values below 30 indicate relatively slower decay phases. Current RSI: 68.57

Trading Deacy Applications

Premium Change analysis serves multiple trading purposes, from position entry timing to exit strategy optimization. Understanding these applications helps traders maximize their options trading effectiveness.

Trading Strategy

Premium Change Signal

Action

Risk Consideration

Long Straddle Entry

High decay RSI + low volatility

Wait for volatility expansion

Time decay acceleration risk

Short Straddle Entry

Low decay RSI + high premiums

Sell elevated premiums

Unlimited loss potential

Position Exit Timing

Accelerating decay patterns

Close losing positions early

Opportunity cost of early exit

Adjustment Triggers

Extreme premium imbalances

Roll or hedge positions

Additional transaction costs

Advanced Premium Analysis Strategies

Sophisticated traders can enhance their Premium Change analysis through advanced techniques that provide deeper market insights and more precise timing signals.

Multi-Timeframe Analysis

1 or 2-Minute Precision Tracking: Ultra-short-term premium movements for scalping opportunities and precise entry timing

3 or 5-Minute Trend Identification: Medium-term premium trends that help identify sustainable directional moves

10 or 15-Minute Pattern Recognition: Longer-term premium patterns that reveal institutional activity and major market shifts

Risk Management Through Premium Monitoring

Continuous premium change monitoring provides essential risk management capabilities, allowing traders to respond quickly to adverse market movements and protect their capital.

Risk Alert System: Set up alerts for extreme premium changes (±50 points from baseline) to catch major market movements early and adjust positions before significant losses occur.

Premium-Based Stop Loss Strategies

Absolute Premium Loss Limits: Set maximum acceptable premium loss amounts based on account size and risk tolerance

Percentage-Based Stops: Use percentage-based stop losses relative to initial premium paid for position sizing consistency

Time-Decay Adjusted Stops: Modify stop loss levels based on expected time decay to avoid premature exits

Volatility-Adjusted Risk Management: Adjust risk parameters based on current volatility environment and premium decay patterns

Key Takeaway: Premium Change analysis with 9:15 AM baseline reference provides traders with comprehensive insights into options pricing dynamics. By monitoring real-time premium movements, combined decay patterns, and RSI indicators, traders can make more informed decisions about position entry, management, and exit timing while maintaining effective risk control.

Conclusion: Premium Change Strategies

Premium Change Divergence: CE premium decreased (-57.10) while PE premium increased (+50.10) → indicates bearish bias.

Combined Premium Decay Negative: At -7, meaning overall premium is reducing → suggests time decay effect favoring sellers.