A "Rolling straddle" in options trading is a strategy where you periodically close and re-open a straddle with a new, later expiry date, essentially resetting your bet on a significant price movement.

What is a Rolling Straddle?

A rolling straddle is an advanced options strategy that involves continuously adjusting straddle positions as market conditions change. The strategy aims to capture volatility while managing time decay and directional risk through systematic position adjustments.

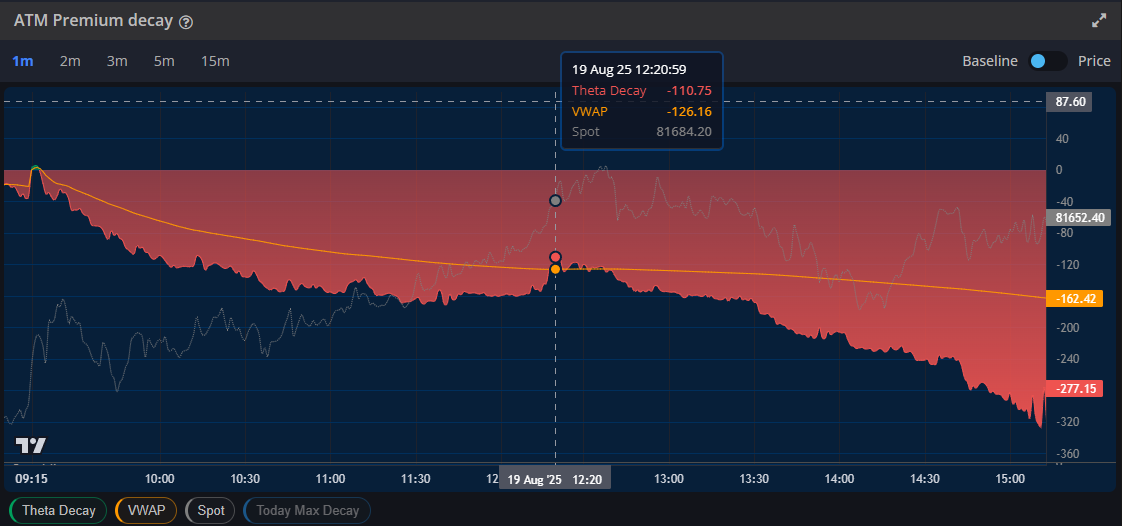

Rolling Straddle Chart with VWAP, EMA, Delta, Z-Score, RSI, Premium Decay, Call Put Price, OI, ATM Strike, Vega and Theta.Rolling Straddle ATM decay Chart: Chart show how many point already decay today.

The straddle chart reveals several critical patterns that traders should monitor closely. The current straddle price of 137.15 shows the market's assessment of volatility premium, which is trading below both the VWAP and EMA levels, suggesting potential undervaluation.

Key Observations from Chart Analysis:

Declining Trend: The straddle has shown a consistent downward trend from higher levels, indicating decreasing volatility premiums

Support Levels: Current price action suggests testing of significant support around the 111-120 range

Volume Pattern: Increased trading activity during price declines indicates active profit-taking or hedging

Technical Indicators: RSI at 44.21 suggests the instrument is approaching oversold territory

Greeks Analysis

Understanding the option Greeks is essential for straddle trading success. The current metrics provide insight into how the position will behave under different market scenarios:

Greek

Current Impact

Trading Implication

Delta Neutral

Approximately 0

Position profits from large moves in either direction

Gamma Exposure

High at ATM strikes

Accelerating profits with significant price movements

Theta Decay

-38.60 (from premium decay chart)

Time decay working against the position

Vega Sensitivity

Positive exposure

Benefits from volatility expansion

Rolling Straddle Chart with EMA, IV, ATM Strike, Z-score and RSI.

ATM Premium Decay Analysis

The ATM Premium Decay chart illustrates the critical time decay component affecting straddle positions. The current decay rate of -38.60 represents the daily premium erosion that traders must overcome through volatility or directional moves.

Premium Decay Patterns

The premium decay visualization shows several important characteristics that impact straddle profitability:

Accelerating Decay: Premium decay intensifies as expiration approaches, particularly in the final weeks

Volatility Impact: Higher implied volatility periods show slower decay rates

Weekend Effect: Time decay continues over market closures, affecting Monday opening positions

Risk Management Alert: The current decay rate suggests that the underlying asset needs to move more than 3.5% from current levels to overcome daily time decay, making this a high-risk, high-reward scenario.

Market Sentiment Indicators

Volatility Environment

The current volatility environment, as indicated by the IV VWAP of 12.01, suggests relatively low volatility expectations. This creates both opportunities and risks for straddle positions:

Volatility Trading Considerations:

Low IV Environment: Current implied volatility levels may present buying opportunities if volatility expansion is expected

Historical Comparison: Comparing current IV to historical ranges helps assess relative value

Event Risk: Upcoming earnings, economic announcements, or geopolitical events can trigger volatility spikes

Volatility Clustering: Periods of low volatility often precede periods of high volatility

Technical Indicator Summary

The combination of technical indicators provides a comprehensive view of market conditions:

Indicator Type

Current Reading

Signal Strength

Trading Bias

RSI

44.21

Moderate

Approaching Oversold

Price vs EMA

Below EMA

Strong

Bearish Bias

Price vs VWAP

Below VWAP

Moderate

Institutional Selling

Volume

Elevated on Declines

Strong

Distribution Pattern

Rolling Straddle Chart Interpretation Guide

Multi-Timeframe Analysis

The rolling Straddle chart displays various timeframes for comprehensive analysis:

3m: Tactical adjustments - Position management decisions

5m: Standard analysis - Primary trading timeframe

15m: Trend confirmation - Broader market context

Position Sizing and Capital Allocation

Effective straddle trading requires disciplined risk management approaches that account for the unique characteristics of volatility trading:

Portfolio Allocation: Limit straddle positions to 2-5% of total trading capital

Diversification: Spread risk across multiple expiration dates and underlying assets

Liquidity Requirements: Ensure adequate cash reserves for position adjustments

Correlation Analysis: Avoid concentrated exposure to highly correlated instruments

Rolling Strangle Chart with VWAP, OI, Call Put Price, IV, Theta.

Strategic Trading Considerations for Rolling Straddle

Entry Criteria

Volatility Expansion: Enter rolling straddles when implied volatility is below historical averages

Technical Confluence: Look for support/resistance levels that may trigger significant moves

Event Calendar: Time entries around known volatility catalysts

Risk-Reward Ratio: Ensure potential profits exceed time decay and transaction costs

Exit Strategies

Profit Targets: Typically 25-50% of maximum possible profit buying straddle or strangle, 1-1.5% profit selling straddle or strangle.

Time Decay Management: Exit positions with 1-2 weeks remaining to expiration

Volatility Contraction: Close when implied volatility returns to historical high levels

Technical Breakdown: Exit if underlying asset breaks significant support/resistance levels

Risk Management Framework

Risk Factor

Management Technique

Implementation

Time Decay

Position sizing and timing

Avoid holding through final weeks

Volatility Risk

IV rank analysis

Trade in high IV environments

Directional Risk

Delta hedging

Adjust underlying exposure

Liquidity Risk

Strike selection

Choose liquid options contracts

Market Context and Timing

The straddle strategy performs best during specific market conditions:

Optimal Market Conditions

High Volatility Environment: When VIX or volatility indices are elevated

Event-Driven Trading: Before earnings announcements or major economic releases

Market Uncertainty: During geopolitical tensions or policy announcements

Technical Breakouts: At key support/resistance levels

Advanced Rolling Straddle Variations

Calendar Straddles: Using different expiration dates for enhanced flexibility. Diagonal Straddles: Combining different strikes and expiries for customized risk profiles. Ratio Straddles: Employing unequal numbers of calls and puts for directional bias.

Conclusion

The rolling straddle options strategy represents a sophisticated approach to trading volatility rather than direction. Success requires careful analysis of multiple factors including implied volatility, time decay, delta positioning, and market timing.

Z-Score Monitoring: Track Z-Score levels for optimal entry timing

Premium Decay Analysis: Monitor combined premium decay for position health

Multi-Timeframe Approach: Use multiple timeframes for comprehensive analysis

High Volatility Focus: Target high volatility environments for maximum profit potential

Technical Integration: Combine with technical analysis for enhanced precision

By mastering these concepts and utilizing advanced charting tools, traders can effectively implement straddle strategies to capitalize on market volatility while managing associated risks.

This tool is available as part of the subscription. Please Click here to subscribe.