In a calendar strategy, you sell the near-term option with higher IV and buy the longer-term option with lower IV. This setup benefits from faster time decay in the short leg while the long leg retains more value.

Calendar Comparison Analysis

Calendar Comparison is a sophisticated analytical tool that compares implied volatility (IV) across different expiration dates for the same underlying asset. This powerful technique helps traders identify optimal entry and exit points for calendar spread strategies by analyzing the volatility term structure and time decay patterns.

Understanding Calendar Comparison

Calendar Comparison analysis involves examining the relationship between near-term and far-term implied volatility to identify trading opportunities. By comparing IV across different expiration cycles, traders can spot potential mispricings and structure profitable calendar spread positions.

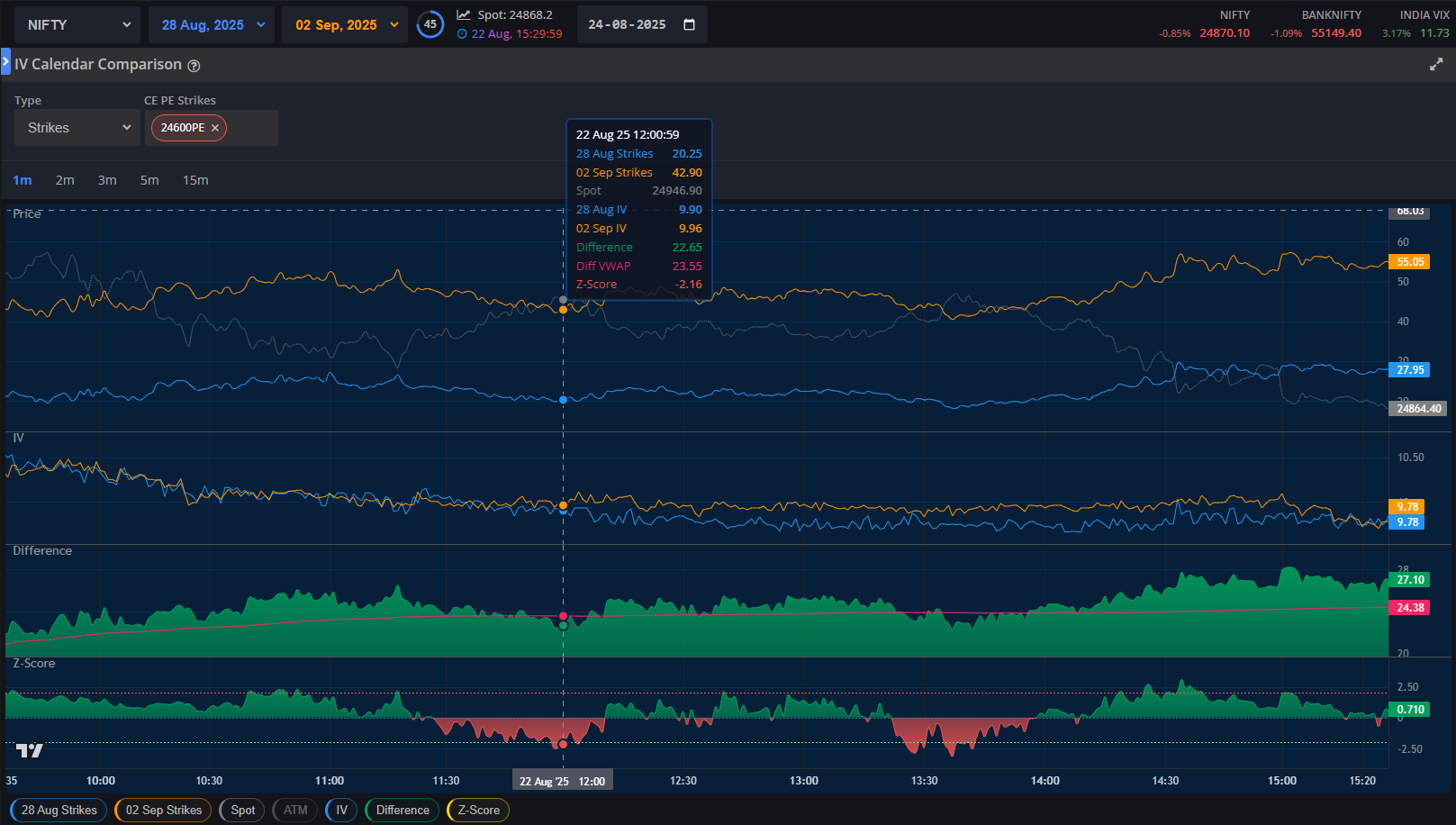

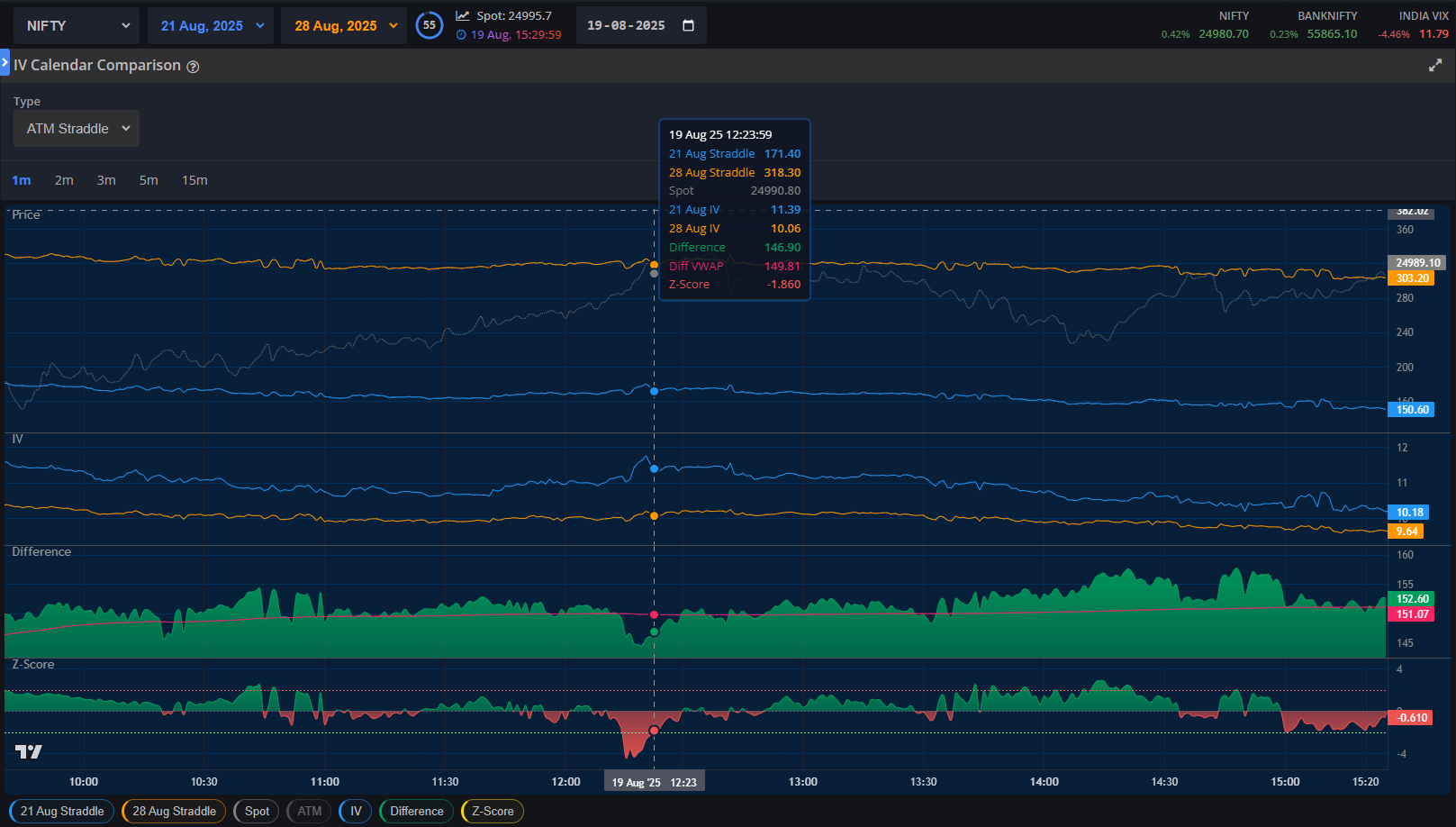

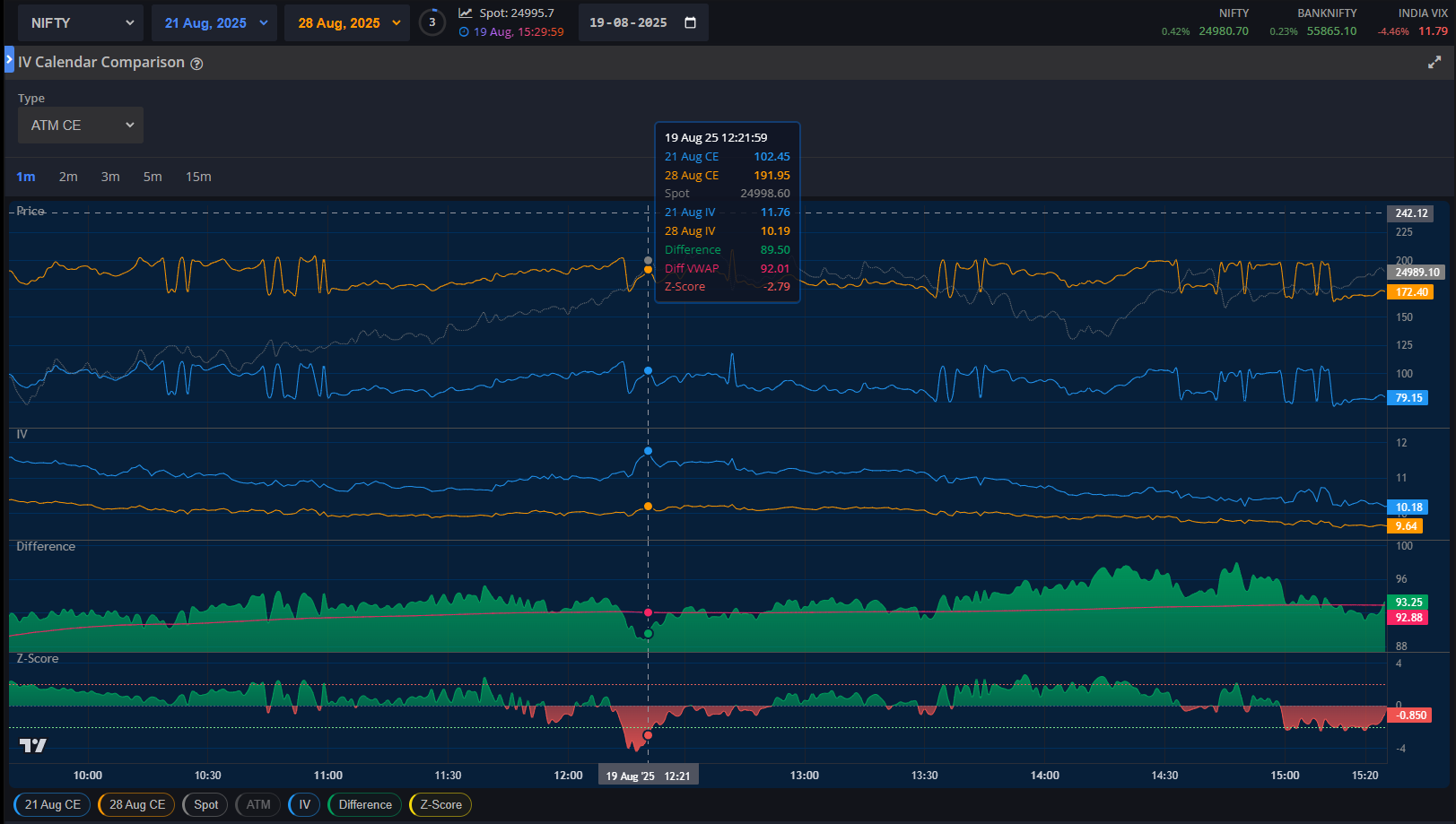

Calendar Comparison: Selected Strikes, IV, calendar difference, Z-score.Calendar Comparison: Rolling ATM call and put, IV, calendar difference, Z-score.

Calendar Spread Analysis

Key Components of Calendar Analysis

Near-Term Expiration IV: The implied volatility of options expiring in the immediate term (typically 1-2 months)

Far-Term Expiration IV: The implied volatility of options expiring in longer periods (typically 3-6 months)

IV Difference: The spread between far-term and near-term implied volatility levels

Z-Score Analysis: Statistical measure showing how far the current IV difference deviates from historical norms

Calendar Spread Mechanics

A calendar spread involves selling a near-term option and buying a far-term option with the same strike price. The strategy profits from time decay acceleration in the near-term option while maintaining exposure to potential volatility expansion in the far-term option.

Strategy Component

Position

Time Decay Impact

Volatility Impact

Near-Term Option

Short (Sell)

Accelerated decay benefits position

IV decrease benefits position

Far-Term Option

Long (Buy)

Slower decay hurts position less

IV increase benefits position

Net Position

Calendar Spread

Benefits from time decay differential

Benefits from volatility term structure normalization

Calendar Comparison: Rolling ATM call, IV, calendar difference, Z-score.

Optimal Entry Conditions

Successful calendar spread trading requires identifying the right market conditions. The Calendar Comparison chart helps traders spot these opportunities through several key indicators.

Entry Signal Analysis

Critical Divergence Patterns:

Z-Score Above +2.0: Indicates the IV difference is significantly above historical norms, suggesting potential mean reversion opportunity

Stable Underlying Price Action: Calendar spreads perform best when the underlying stays near the strike price

Time to Expiration Sweet Spot: Optimal when near-term has 1 week and far-term has 15-30 days remaining

Low Historical Volatility Environment: Reduces risk of significant underlying price movements that could hurt the position

Risk Management Strategies

Calendar spreads require active management due to their sensitivity to both time decay and underlying price movement. Understanding the risk profile helps traders make informed decisions.

Pro Tip: Monitor the position's delta closely. As the underlying moves away from the strike price, the calendar spread can quickly shift from profitable to losing territory.

Key Risk Factors

Risk Factor

Impact on Position

Management Strategy

Large Price Movements

Both options move away from optimal zone

Close position or roll strikes

Volatility Collapse

Far-term option loses value faster

Consider early exit or defensive adjustments

Time Decay Acceleration

Near-term decay overwhelms far-term

Monitor theta decay rates daily

Early Assignment Risk

Short option assigned before expiration

Close or roll positions before ex-dividend dates

Advanced Calendar Strategies

Experienced traders can enhance calendar spread performance through various advanced techniques and modifications.

Double Calendar Spreads: Implementing both call and put calendars at different strikes to create a wider profit zone

Diagonal Spreads: Using different strikes for near-term and far-term options to adjust directional bias

Rolling Strategies: Systematically rolling the near-term option to maintain optimal time decay advantage

Volatility-Based Adjustments: Modifying positions based on implied volatility changes rather than just price movement

Market Conditions and Performance

Calendar spreads perform differently across various market environments. Understanding these patterns helps traders time their entries and exits more effectively.

Optimal Market Conditions: Calendar spreads typically perform best in low-volatility, sideways-trending markets where the underlying asset trades within a narrow range around the chosen strike price.

Performance Across Market Cycles

Low Volatility Periods: Time decay becomes the primary profit driver as volatility remains subdued

Rising Volatility Environments: Far-term options benefit more than near-term, improving spread profitability

Volatile Markets: Increased risk of underlying moving beyond profit zones, requiring active management

Trending Markets: Directional movement can quickly erode calendar spread value, necessitating defensive actions

Key Takeaway: Calendar Comparison analysis provides traders with a systematic approach to identifying and managing calendar spread opportunities. By understanding the relationship between near-term and far-term implied volatility, traders can make more informed decisions about when to enter, adjust, or exit these complex strategies.

Conclusion: Calendar Strategies

Big Price Difference Between Expiries: Calendar Spread Opportunity

IV is Almost Flat: Neutral IV environment, Neutral Calendar, focus on time decay.

Difference Increasing Throughout the Day: Mean Reversion Play, Reverse Calendar Spread if expecting reversion.

Z-Score Swings Around 0 but Turns Negative Midday: Standard Deviation Signal, Buy Calendar Spread when Z-score < -1, exit near 0 or positive.

Spot Stayed in Range: Range-bound market, Double Calendar Spread for balanced theta decay.

Time Decay Advantage: Theta Harvesting, Put Calendar Spread or Diagonal Put Spread if slight bearish bias.

This tool is available as part of the subscription. Please Click here to subscribe.